Theme: Economic Growth, Job Creation, Strong Middle Class

When the new government said last year that it would return Canada to deficits, few expected the numbers to jump to nearly $30 billion this year and next and add $100 billion in debt over the next five years. But lower-than-expected revenues have forced the government’s hand, according to Finance Minister Bill Morneau, requiring increased spending to stimulate the sluggish economy and support the middle class.

World economic growth is expected to be 3% this year and this slow growth presents challenges for Canada as 50% of our exports are commodity related. Relatively strong US growth will help Canada as 75% of our exports are to the USA, US household growth (the number of new households being created each year) is expected to be in the range of 1,240,000 per year from 2015 to 2025, up significantly from 965,918 per year from 2010 – 2013. New household formation has a very strong impact on the US economy as it creates demand for new housing and all the goods and services (carpeting, appliances, legal services, insurance, etc.) related to home construction.

There were no major personal tax changes in this budget, other than a revamping of the system of child benefits.

The budget documents included for the first time a separate chapter dedicated to Indigenous people. Raising the priority of First Nations issues is consistent with the Liberal’s election campaign promises and may signal a new “chapter” in our relations with Canada’s First Nations.

Building — and Spending — for Growth

In part, the Federal Government hopes to build its way to economic growth, spending $12 billion over five years on a range of infrastructure projects including public transit, affordable housing, water management for First Nations communities, climate change mitigation, early learning and childcare. The government predicts these investments will increase Canada’s GDP by 0.2 per cent this year and 0.4 per cent in 2017.

The Liberals propose $120 billion in infrastructure spending over 10 years. The plan for the remaining funds is expected later this year.

The bulk of the proposed additional program spending in the 2016 budget focuses on families, seniors, veterans, health care, post-secondary education, innovation and clean energy. These measures also aim to encourage growth or restore benefits eliminated by the previous government.

To balance all this spending, the government plans to close a number of domestic and international loopholes that permit organizations and individuals to avoid or defer tax, and provide the Canada Revenue Agency with $800 million over five years for compliance initiatives. Taxpayers should expect greater tax audit activity, especially focused audit initiatives, and more aggressive collection activity by Canada Revenue.

On top of these preliminary measures to limit tax evasion and deferral, the government has proposed a review of the tax system to reduce or eliminate inefficient tax measures. We would expect further announcements later in the year as the government progresses through its review.

Key Personal Measures

As noted in the government’s December 2015 update, the second marginal income tax rate has decreased from 22 per cent to 20.5 per cent and a new top tax rate of 33 per cent has been added for incomes above $200,000.

The government also returned the TFSA contribution limit to $5,500 (from $10,000) and promised to index the limit to inflation.

Beginning July 2016, the new Canada Child Benefit (CCB) will provide up to $6,400 for each child under age 6 and up to $5,400 for children aged 6–17. Only families with incomes below $30,000 per year will receive the full benefit. The CCB will replace the Canada Child Tax Benefit and Universal Child Care Benefit.

The family tax cut credit for families with at least one child under 18 at home and the children’s fitness and arts tax credits will also be eliminated.

Key Budget Measures for Business

The small business tax rate will remain at 10.5 per cent. The former government had scheduled regular decreases in the rate over the next few years, but Morneau has put those changes on hold. Business owners will also face stricter rules with regard to using partnerships or corporations to multiply access to the small business deduction and avoid tax.

The Eligible Capital Property (ECP) regime will be repealed and ECP will fall under a new Capital Cost Allowance class with a 100 per cent inclusion rate and 5 per cent annual depreciation rate. The transition will begin January 2017.

Measures That Were Not Introduced

The Budget did not propose a number of measures that were either specifically mentioned in earlier government documents or that were speculated about in the community.

A statement made by the current Liberal government during the fall election campaign indicated that the 50 per cent reduction in the amount included in income in connection with certain stock option benefits would be limited to $100,000 of benefits realized in a particular year. The Budget made no mention of this measure.

There was speculation that the portion of a capital gain that would be taxable would be increased above the present 50 per cent inclusion rate. No such measure was introduced.

There was also speculation that the income earned by certain service corporations (such as professional corporations) would not be eligible for the small business deduction (SBD) unless the corporation had a certain minimum number of employees. No such measure was introduced.

The April 2015 Budget proposed an exemption from capital gains tax with respect to certain dispositions of private company shares and real estate where the cash proceeds are donated to a charity within 30 days after the disposition and the private company shares or real estate are sold to a purchaser who deals at arms-length with both the donor and donee. This proposal has been dropped.

Personal Tax Measures

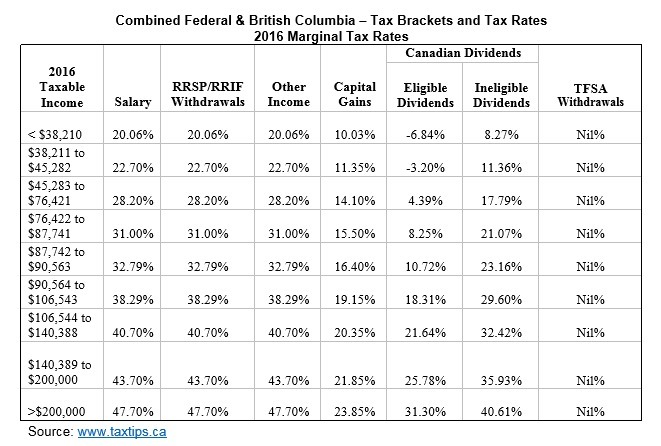

2016 BC Personal Marginal Tax Rates

The personal tax rates for 2016 are:

Dividends and capital gains continue to be taxed on a more favorable basis than interest income. Capital gains are only taxed when realized; unrealized capital gains compound on a tax-deferred basis until sold.

Funds withdrawn from registered accounts (RRSP/RRIF) are taxed at your marginal tax rate.

All income earned inside Tax Free Savings Accounts (TFSA) is tax free and withdrawals are permitted with no tax consequences. Withdrawals renew the annual allowable contribution amount so whatever you withdraw may later be re-invested back into the TFSA.

Canada Child Benefit

A non-taxable Canada Child Benefit (CCB) will replace the Canada Child Tax Benefit (CCTB) and Universal Child Care Benefit (UCCB) assistance programs effective July 1, 2016.

Akin to the CCTB and UCCB, the new CCB will provide financial assistance in the form of monthly payments to families with children under the age of 18. A maximum benefit of $6,400 will be provided for each child under the age of 6 and $5,400 for children aged 6 to 17. These maximums begin to phase out where the adjusted family net income is between $30,000 and $65,000. The phase-out rates in this threshold range from 7 per cent for a one-child family up to 23 per cent for a family with 4 or more children. Once adjusted family net income exceeds $65,000, any remaining benefit is phased out at slower rates ranging from 3.2 per cent to 9.5 per cent.

The Budget broadens the definition of an eligible individual for purposes of the CCB to include an Indian within the meaning of the Indian Act provided that all other criteria under the definition are met.

Also beginning July 1, 2016, the children’s special allowance is proposed to be increased to the same level as the CCB so that children in child protection agencies are treated consistently.

Family Tax Cut Credit

For the 2016 taxation year and beyond, the Budget proposes to eliminate the Family Tax Cut Credit that currently permits limited income splitting for couples with at least one child under the age of 18.

This credit allows a higher-income earning spouse or common-law partner to notionally transfer up to $50,000 of taxable income to their spouse or common-law partner in order to reduce the couple’s combined tax liability by a maximum of $2,000.

Children’s Fitness and Arts Tax Credits

The government proposes to halve the maximum eligible expenditures on which the 15 per cent refundable Children’s Fitness and Art Tax Credits can be claimed in the 2016 taxation year, and will eliminate the credits in 2017.

In particular, the Budget proposes to reduce the Children’s Fitness Credit maximum eligible amount from $1,000 to $500 in 2016 and eliminate it in 2017. The maximum eligible amount for the Children’s Arts Tax Credit would be reduced from $500 to $250 in 2016 and, again, eliminated in 2017.

Education and Textbook Tax Credit

Effective January 1, 2017, the Budget proposes to eliminate the 15 per cent non-refundable Education and Textbook Tax Credits. Unused education and text book credits carried forward from prior to 2017, will remain available to be claimed in 2017 and subsequent years.

The government plans to use the resulting tax savings to increase the Canada Student Grant amounts. These grants are available to undergraduate students from low and middle income families who apply and qualify for student financial assistance.

The 2016 budget is increasing the Canada Student Grant amounts by 50%:

- from $2,000 to $3,000 per year for students from low-income families;

- from $800 to $1,200 per year for students from middle-income families; and

- from $1,200 to $1,800 per year for part-time students

These higher grant amounts will be available for the 2016-2017 academic year.

Teacher and Early Childhood Educator School Supply Tax Credit

The Budget proposes to introduce the new Teacher and Early Childhood Educator School Supply Tax Credit, a 15 per cent refundable credit based on the amount of expenditures, up to a maximum of $1,000, made for eligible supplies purchased on or after January 1, 2016.

The credit is available to eligible educators who are teachers or early childhood educators that hold a valid certificate recognized by the province or territory in which they are employed. The credit cannot be claimed on expenditures claimed under any other provision of the Income Tax Act.

Top Marginal Tax Rate — Further Consequential Amendments

On December 7, 2015, the government announced that it will reduce the personal income tax rate in the second bracket from 22 per cent to 20.5 per cent in the 2016 taxation year. A new top tax bracket of 33 per cent on taxable income over $200,000 will be introduced as well.

The Budget proposes consequential amendments further to those already included in Bill C-2 which was tabled on December 9, 2015. These include the following:

- Personal services business income earned by corporations will be subject to a 33 per cent tax rate, up from the previous rate of 28 per cent;

- A reduction of the “relevant tax factor” under the foreign affiliate rules from 2.2 to 1.9;

- On donations in excess of $200, a 33 per cent donation tax credit will be available to trusts that are subject to the 33 per cent rate on all their taxable income;

- Excess contributions to employee profit sharing plans will be subject to the 33 per cent tax rate.

The above amendments are proposed to take effect in the 2016 taxation year.

Ontario Electricity Support Program

This program, which took effect on January 1, 2016, provides relief to low-income households for the cost of electricity via a monthly credit on a taxpayer’s electricity bill. The Budget proposes to exclude such credits from a taxpayer’s income so that other benefits subject to income threshold tests are not adversely impacted.

Northern Residents Deductions

The Budget proposes to increase the maximum Northern Resident Deduction from $8.25 to $11 per day for each member of a household that resides in a Northern Zone for at least six consecutive months beginning or ending in a particular taxation year. In cases where only one member of a household claims the deduction, the increase is proposed to be from $16.50 to $22 per day.

Taxpayers resident in an Intermediate Zone can only deduct half of the aforementioned amounts.

Mineral Exploration Tax Credit

Eligibility for the Mineral Exploration Tax Credit is proposed to be extended for one year under the Budget. That is, the credit will apply to flow-through share agreements entered into on or before March 31, 2017.

Labour-Sponsored Venture Capital Corporation (LSVCC) Tax Credit

The Budget proposes to reestablish the 15 per cent tax credit for a purchase of shares of a provincially registered LSVCC for the 2016 taxation year and beyond. However, the Budget does not reestablish the tax credit for a federally registered LSVCC; the credit will remain at 5 per cent in 2016 and will be eliminated in 2017.

Taxation of Switch Fund Shares

In general terms, a mutual fund corporation that is a “switch fund” allows its shareholders to exchange their shares for another class of shares in order to change their economic exposure to a different fund of the corporation. The provisions of the Income Tax Act currently deem such an exchange to not be a disposition.

The Budget proposes to treat such an exchange after September 2016 as a fair market value disposition.

Sale of Linked Notes

A linked note is a debt obligation that provides its holder with a return based on the performance of an index or reference asset. The underlying index or reference asset is normally unrelated to the business activities of the linked note issuer.

Investors that hold link notes as capital property have used a strategy whereby they sell their linked notes in advance of their maturity in order to get capital gains treatment on any appreciation as opposed to fully taxable deemed interest. The logic behind this strategy is that there is no deemed interest accrual rules that govern prescribed debt obligations because the maximum amount of interest is not determinable at the time of the sale. That is, interest can only be accrued and included in income when the amount becomes determinable, which is usually very near to maturity.

The Budget proposes to amend the prescribed debt obligation provisions to deem any gain on the sale of linked notes after September 2016 to be interest income.

Business Income Tax Measures

Small Business Tax Rate

The federal small business reduction will remain at 17.5 per cent for 2016 and subsequent taxation years, which provides for a federal small business tax rate of 10.5 per cent, down from 11.0 per cent in 2015. Of course, the provincial rate must be added to determine the actual rate.

The related dividend gross-up of 17 per cent for other than eligible dividends and the dividend tax credit of 21/29 of the gross-up will remain for 2016 and subsequent taxation years. Consequently, the prior proposals to further increase the SBD rate and reduce the related small business tax rate for 2017 and subsequent taxation years, along with the consequential changes to the dividend gross-up and dividend tax credit, will not be going ahead.

Multiplication of the Small Business Deduction

The current specified partnership income rules are intended to prevent the multiplication of the SBD where a corporate partnership is utilized since each corporate partner is only entitled to an SBD equal to its share of the partnership’s active business income multiplied by $500,000. Structures have been implemented to circumvent these rules through the utilization of a separate Canadian-controlled private corporation (CCPC) which is not a member of the partnership. Such corporation (which would be owned by the shareholder of one of the corporate partners or by a person who is not at arm’s-length with the shareholder) would be paid by the partnership for services provided.

The Budget proposes to deem this separate CCPC to be a member of the partnership, which in effect, causes the active income earned by this CCPC from services billed to the partnership to still be subject to its prorated share of the annual SBD.

Similar rules will apply where a CCPC provides services or property to certain private corporations rather than to a partnership as in the above example. The income so earned by the CCPC will be ineligible for the SBD where, at any time during the year, the CCPC, one of its shareholders or a person who does not deal at arm’s length with such a shareholder has a direct or indirect interest in the private corporation.

These proposals generally apply to taxation years which begin on or after Budget Day. In addition, these proposals do not apply to a CCPC all or substantially all of the active income of which is from providing services or property to arm’s-length persons other than the partnership.

Currently, certain investment income, such as rent or interest, earned by a CCPC, from an associated CCPC that deducts the payments from its own active income, is treated as active income rather than investment income. In addition, two CCPCs, which are not normally associated with each other are considered to be associated by being associated with the same “third” corporation. Although these two CCPCs can elect not to be associated for SBD purposes, the above rule which treats certain investment income to be active rather than passive still applies.

The Budget proposes to retain the character of the investment income in the hands of the recipient as investment income rather than deeming it to be active income where the “third company” election not to be associated is utilized. In addition, where the “third company” election not to be associated is utilized, the third company will continue to be associated with each of the other two CCPCs for purposes of applying the $10 – 15 million taxable capital limit for SBD purposes.

Tax on Personal Services Business Income

Effective January 1, 2016, the federal tax rate on personal services business income will be increased by 5 per cent (from 28 per cent to 33 per cent) to correspond with the increase in the top federal marginal personal tax rate to 33 per cent on taxable income over $200,000 for 2016 and subsequent years. The rate increase will be prorated for taxation years which straddle January 1, 2016.

Consultation on Active versus Investment Income

The consultation resulting from the 2015 Budget to review the circumstances in which income from property should qualify as active business income was completed in August 2015. The Budget did not introduce any changes to these rules.

Distributions Involving Life Insurance Proceeds

The Budget proposes measures to ensure that the addition to the capital dividend account (CDA) for private corporations and the adjusted cost base for partnership interests, on the death of an individual insured under a life insurance policy, is reduced by the adjusted cost basis of the policy. This will be the case whether or not the corporation or partnership that receives the policy benefit is the policyholder and therefore the premium payer. In addition, information reporting requirements will apply where a corporation or partnership is not a policyholder, but is entitled to receive a policy benefit. This measure will apply to policy benefits received as a result of a death that occurs on or after Budget Day.

Transfers of Life Insurance Policies

Currently, where a policyholder disposes of their interest in a life insurance policy to a non-arm’s-length person (to a corporation for example), the policyholder’s proceeds are deemed to be equal to the cash surrender value (CSV) of the policy at the time notwithstanding the fact that the fair market value (FMV) of the policy, and therefore the consideration received by the transferor, might be higher. The policyholder would be taxable only to the extent that the CSV exceeds the adjusted cost basis of the policy at the time; any excess of the FMV of the policy over the CSV is not currently taxable. In addition, this excess of FMV over the adjusted cost basis can later be effectively extracted through the corporation’s CDA. Similar concerns arise in the partnership context and where a policy is contributed to a corporation as capital.

The Budget proposes that the policyholder’s proceeds in the above scenario would be the FMV of the policy rather than its CSV. Consequently, any excess of the FMV over the adjusted cost basis would be taxable. This measure will apply to dispositions on or after Budget Day.

The Budget also proposes to amend the CDA rules for private corporations and the adjusted cost basis computation for partnership interests where the interest in the policy was disposed of before Budget Day for consideration in excess of the CSV of the policy. This amendment, which in essence amounts to retroactive taxation, will reduce the addition to the corporation’s CDA or adjusted cost base of an interest in a partnership by the amount of such excess which will result in tax when the funds are withdrawn from the company. Consequently, additional funds would be required to pay these taxes, a cost not anticipated when the policy was transferred to the company. This measure will apply in respect of policies under which policy benefits are received as a result of deaths occurring on or after Budget Day.

Valuation of Derivatives

Inventory is generally valued at the end of the year at the lower of its cost and FMV, which provides for a write-down to the extent that the FMV is less than the cost at year-end. However, accrued gains on inventory are not recognized until sold. Although there is generally no concern with conventional types of inventory, the potentially long-term holding period for derivatives is a concern to the Department of Finance. Consequently, the Budget proposes to exclude certain derivatives as inventory to preclude the utilization of the above valuation method to create a current write-down. This measure will apply to derivatives entered into on or after Budget Day.

Debt Parking to Avoid Foreign Exchange Gains

Where a foreign currency debt is on capital account, any applicable foreign exchange gain is not realized by the debtor until the debt is settled or extinguished. In order to avoid realizing the foreign exchange gain on the repayment of the debt, some taxpayers have entered into debt-parking transactions where a non-arm’s-length person would acquire the debt from the lender. The current debt-parking tax rules do not take into account the foreign exchange gain realized on the debt. The Budget proposes to introduce rules so that any accrued foreign exchange gains on foreign currency debt will be realized when the debt becomes a “parked obligation”. This measure will generally apply to a foreign currency debt which becomes a parked obligation on or after Budget Day.

Eligible Capital Property

The 2014 federal budget announced that the existing rules that related to both the acquisition and disposition of eligible capital property (ECP) (such as goodwill) would be reviewed.

At the present time, 75 per cent of the cost of ECP is added to the cumulative eligible capital (CEC) pool which is amortized at the rate of 7 per cent per annum of the declining balance. The proceeds of disposition of ECP are first credited to the CEC pool, if any, and previous deductions are recaptured. 50 per cent of the balance is treated as active business income (and 50 per cent falls into the CDA). The effective tax rate is therefore half of the small business rate and/or half of the general rate applicable to active business income.

Note that each of the provinces imposes its own provincial rate. So, for example, in Ontario, the rate applicable to the small business income portion would be 7.50 per cent (50 per cent of 15.0 per cent) and 13.25 per cent (50 per cent of 26.5 per cent) on the non-small business portion; in British Columbia, the rate applicable to the small business income portion would be 6.50 per cent (50 per cent of 13.0 per cent) and 13.00 per cent (50 per cent of 26.0 per cent) on the non-small business portion.

Ignoring the lack of a reserve for deferred proceeds on the sale of goodwill, this treatment has, initially, been more attractive than the result of treating the gain as a capital gain which is taxed at 50 per cent of the high corporate rate applicable to investment income resulting in an effective rate of approximately 25 per cent.

The Budget introduces a new regime that will be effective on January 1, 2017.

The new rules will add 100 per cent of the cost of what has heretofore been classified as ECP to a new capital cost allowance (CCA) class, Class 14.1, which will be depreciated at the rate of 5 per cent of the declining balance per annum. 100 per cent of the proceeds of disposition of this type of property will be credited to the pool in accordance with the existing rules applicable to dispositions of depreciable property.

Transitional rules will transfer December 31, 2016 CEC pool balances to Class 14.1. For 10 years, pre-2017 balances will be depreciated at the rate of 7 per cent of the declining balance per annum. Small businesses will benefit from more generous write-offs for minor expenditures. For example, the first $3,000 of the cost of incorporation will be deductible as a current expense.

Accelerated Capital Cost Allowance

The Budget proposes to expand CCA Classes 43.1 and 43.2 to include electric vehicle charging stations and electric energy storage equipment acquired on or after Budget Day that would otherwise be included under CCA Class 8. This would provide tax deferral as Classes 43.1 and 43.2 provide for CCA at rates of 30 per cent and 50 per cent, respectively, on a declining-balance basis, while Class 8 only provides a declining-balance rate of 20 per cent.

Charging stations that supply less than 90 kilowatts of power would be included in Class 43.1, while stations that supply 90 kilowatts or more would be included in Class 43.2.

Electric energy storage equipment that is part of an electricity generation system that is eligible for Class 43.1 or 43.2 will be included in the same class as the system. Standalone electrical storage equipment may also be eligible for Class 43.1 or 43.2 treatment if certain criteria are met.

Emission Trading Regimes

Governments may require emitters of regulated substances such as greenhouse gases to remit emissions allowances to them. Such allowances can be supplied by the government, purchased in a market, or earned based on emission-reducing activities.

Current tax rules do not specifically address emission allowances. The Budget proposes to provide guidance to treat emission allowances as inventory for taxation years beginning after 2016. Also, these rules would apply to emission allowances acquired in taxation years ending after 2012 if so elected by a taxpayer. Due to the high volatility of such allowances, inventory valuation under the lower of cost and net realizable method would not be permitted.

International

In the domestic context, section 84.1 is designed to prevent surplus stripping in non-arm’s-length situations. The following broad example illustrates this provision.

Assume that individual X, a Canadian resident, owns all of shares of Opco, a corporation resident in Canada, having an FMV of $100,000, an adjusted cost base (ACB) of $20,000 and paid-up capital (PUC) of $1.00. If X were to transfer the shares of Opco to a non-arm’s-length Holdco and did not wish to realize a taxable amount, X could receive non-share consideration with a maximum FMV of $20,000, being the greater of the ACB ($20,000) and the PUC ($1.00). This would be true even if the gain on the disposition were sheltered by the capital gains exemption. If X were to receive, say, a note of $100,000, X would be deemed to have received a dividend of $80,000. If X were to receive shares of Holdco with a PUC of $100,000, the PUC would be ground down to $20,000 to prevent the tax-free extraction of surplus.

If X were a non-resident (whether an individual or a corporation (Forco)), section 212.1 would operate in a similar, but not identical fashion.

If X were to receive non-share consideration with an FMV greater than the $1.00 PUC (not the $20,000 ACB), from a Holdco resident in Canada, X would be deemed to have received a dividend equal to the excess. While a capital gain on the disposition would not have been taxed in Canada unless the shares were “taxable Canadian property” (and even then only if the gain was not exempted by a tax treaty), the deemed dividend would be subject to Canadian withholding tax.

If X were to receive shares of Holdco with an FMV greater than the $1.00 PUC (not the $20,000 ACB), the PUC would be ground down to $1.00 to prevent the tax-free extraction of surplus.

Subsection 212.1(4) provides an exception to section 212.1 where a Forco disposes of shares of Opco to a Holdco that controls Forco. The Department of Finance feels that this exception has been abused. As a consequence, with respect to dispositions on or after Budget Day, the exception in subsection 212.1 will not apply where Forco owns, directly or indirectly, shares of Holdco and does not deal at arm’s-length with Holdco.

Transfer Pricing

Section 247 contains rules to ensure that cross-border charges among non-arm’s length entities generally reflect prices that would be negotiated by arm’s-length parties. In this regard, certain recommendations of an international study, the Base Erosion and Profit Sharing (BEPS) project, are consistent with existing CRA practices and require no Canadian changes at this time.

The Budget proposes country-by-country reporting requirements that would allow inter-company pricing to be monitored more easily. The new rules will apply to taxation years that begin after 2015, but only to groups with consolidated revenues of at least €750 million.

Treaty Shopping

The BEPS project addressed “treaty shopping,” i.e., the abuse of tax treaty networks whereby an international organization establishes a corporation in a second jurisdiction only for the purpose of taking advantage of a tax treaty between that second jurisdiction and a third jurisdiction.

The Budget indicates that future Canadian tax treaties will contain anti-avoidance provisions to counter such abuses.

Back-to-Back Rules

Subsection 18(6) contains an anti-avoidance measure intended to curtail the avoidance of the “thin capitalization” rules by interposing an ostensibly arm’s-length lender between a Canadian borrowing entity and the real non-arm’s-length lender. A similar anti-avoidance rule is found in subsection 212(3.1) where an attempt is made to avoid Canadian withholding tax on the payment of interest to a non-arm’s-length lender by interposing an ostensibly arm’s-length lender between a Canadian borrower and the real non-arm’s-length lender.

The Budget indicates that Canada will strengthen existing rules to prevent tax avoidance in connection with back-to-back arrangements. The new rules will apply, for example, where back-to-back arrangements are intended to reduce Canadian withholding tax in connection with rents and royalties, to avoid the “upstream loan” rules (where a Canadian corporation receives a loan from a foreign affiliate to avoid receiving a taxable dividend from that affiliate) and in other more complex circumstances.

International Tax Rulings

The Budget confirms that, commencing in 2016, Canada will begin spontaneously exchanging tax rulings with other jurisdictions that agree to do the same.

Sales and Excise Tax Measures

GST/HST

The Budget proposes a number of GST/HST amendments, including the following.

De minimis financial institutions — Under section 149 of the Excise Tax Act (ETA), a person whose revenues from financial activities exceed a minimum threshold may be considered a financial institution for GST/HST purposes. More specifically, a person earning more than $1 million in interest income from bank deposits in a taxation year is generally considered to be a financial institution for the following taxation year.

To allow a person to engage in basic deposit-making activity without incurring such consequences, the Budget proposes to exclude from the determination of the $1 million threshold, interest earned from demand deposits, term deposits, and GICs with a maturity period of less than one year.

This measure applies to a person’s taxation years commencing on or after Budget Day. For the purposes of determining whether a person is required to file Form RC7291 (the Financial Institution GST/HST Annual Information Return), this measure applies to a person’s fiscal year that straddles that date.

Application of GST/HST to cross-border reinsurance — The ETA requires financial institutions with a branch or subsidiary outside Canada to self-assess and remit GST/HST for certain expenses incurred outside Canada that relate to its Canadian activities.

Amendments to the ETA would clarify that the following components of imported reinsurance services would not form part of the tax base that is subject to these self-assessment provisions:

- Ceding commissions, and

- Margin for risk transfer.

In addition, the Budget proposes to set out specific conditions under which the special rules for financial institutions do not impose GST/HST on reinsurance premiums charged by a reinsurer to a primary insurer.

These measures will apply retroactively to any specified year of a financial institution that ends after November 16, 2005.

Transitional rules would allow a financial institution to request a reassessment to determine its tax owing under the GST/HST imported supply rules for a past specified year, but only for the purpose of taking this measure into account. A financial institution will have one year after the date the enacting legislation receives Royal Assent to request a reassessment.

Closely related test — The ETA allows closely related corporations to make group relief elections under certain circumstances to treat supplies between them as if they were made for no consideration.

Generally, this measure will take effect one year after the Budget Day. However, this measure applies as of March 23, 2016, for determining whether the requirements for the closely related test requirements are met for elections under subsection 150(1) and subsection 156(2) of the ETA, where such elections are filed after Budget Day and take effect after that date.

GST/HST on donations to charities — Under current GST/HST rules, if a person makes a donation and receives property or services in return, GST/HST generally applies on the full value of the donation. In contrast, the Income Tax Act allows for “split-receipting.” This allows a charity to provide a donation receipt for the donation amount less any the value of any property or service received by the donor.

The Budget proposes to introduce similar split-receipting rules for the ETA. Specifically, if a charity provides property or services and an income tax receipt may be issued for a portion of the donation, GST/HST applies only to the value of the property or services supplied to the donor.

This measure applies to supplies made after Budget Day. However, transitional relief is available for charities that did not collect GST/HST on the full value of donations for supplies made after December 20, 2002, and on or before Budget Day.

Eligible capital property — As noted above (see Business Income Tax Measures — Eligible capital property), the Budget proposes to repeal the ECP regime and replace it with a new CCA class (Class 14.1), effective January 1, 2017. As a result, all ECP will become capital property under the Income Tax Act.

To ensure the application of GST/HST in this area is not affected, the Budget proposes to amend the definition of capital property under the ETA to exclude property in new Class 14.1. Therefore, property that was ECP under the Income Tax Act will continue to be excluded from capital property for GST/HST purposes. The Budget also makes consequential amendments to the Streamlined Accounting (GST/HST) Regulations.

These amendments will take effect on January 1, 2017.

Health Measures — The Budget proposes to add the following medical and assistive devices to the list of zero-rated medical devices:

- Insulin pens and insulin pen needles, and

- Intermittent urinary catheters, supplied on the written order of a medical doctor, registered nurse, occupational therapist, or physiotherapist for use by a consumer named in the order.

Zero-rating applies to any supplies of insulin pens and insulin pen needles made after Budget Day. In addition, zero-rating applies to any such supplies made on or before the Budget Day, unless the supplier charged, collected, or remitted GST/HST for that supply on or before that date. Zero-rating applies to any supply of an intermittent urinary catheter made after Budget Day.

In addition to the above-listed measures, the Budget amends the ETA to clarify that GST/HST applies to supplies of purely cosmetic procedures provided by all suppliers, including registered charities. This amendment applies to supplies made after Budget Day.

Exported call centre services — Zero-rating will apply to certain exported supplies of call centre services. Specifically, zero-rating will apply to a supply of providing technical or customer support to individuals by means of telecommunications if:

- The supply is made to a non-resident who is not a GST/HST registrant, and

- It is reasonable to expect the technical or customer support will be provided to individuals outside Canada at that time.

This measure applies to supplies of such call centre services made after Budget Day. In addition, zero-rating applies to any such supplies made on or before Budget Day, unless the supplier charged, collected, or remitted GST/HST for that supply on or before that date.

Zero-rating does not apply to supplies of advisory, consulting, or professional services, or a supply of a service of acting as an agent of the non-resident person.

Reporting of grandparented housing sales — Currently, builders are subject to special reporting requirements for housing sales that were “grandparented” for HST purposes. The Budget proposes to limit such reporting requirements to sales of $450,000 or more. In addition, a builder would be entitled to make an election to report all past grandparented housing sales for which the consideration was $450,000 or more, thereby allowing a builder to correct any past misreporting and avoid potential penalties.

Excise Tax

The Budget contains several amendments relating to excise tax levied under the ETA.

Heating oil — Currently, an excise tax exemption applies in respect of diesel fuel that is consumed to produce heat for any purpose, including industrial processes. The Budget proposes to limit relief to diesel oil consumed exclusively to provide heat to a home, building, or similar structure. This measure will generally apply to fuel delivered or imported after June 2016.

Electricity generation — While excise tax generally applies to diesel fuel consumed for motive purposes, an exemption applies for diesel fuel used in or by a vehicle to generate electricity, if certain conditions are met. The Budget proposes to eliminate this exemption. Excise tax will therefore apply to diesel fuel used to produce electricity in any vehicle, regardless of purpose. This measure will generally apply to fuel delivered or imported after June 2016.

Excise Act, 2001

The Budget proposes to enhance certain security and collection provisions in the Excise Act, 2001.

Security — The Excise Act, 2001 requires manufacturers of tobacco products to hold a license. It also requires stamping for all tobacco products destined for duty-paid entry into Canada, thus indicating that duty has been paid. In order to be issued a license or duty-paid stamps, tobacco manufacturers and other persons that import tobacco products must post security with the Canada Revenue Agency (CRA). Currently, the maximum amount of security required

is $2 million.

The Budget proposes to increase the maximum amount of security from $2 million to $5 million. This measure will take effect on the later of:

- The date the enacting legislation receives Royal Assent, and

- The date that is three months after Budget Day.

Collection — Currently, if a person objects to or appeals an assessment of excise duty payable, the CRA may not take collection actions while a decision or judgment is pending. The Budget introduces amendments that would allow the minister to require a person to post security for assessed amounts and penalties exceeding $10 million, to the extent the amount remains uncollected. If the person fails to post security, the minister may take collection action to recover an amount equal to the amount of required security.

These measures apply to amounts assessed and penalties imposed after the day on which the enacting legislation receives Royal Assent.